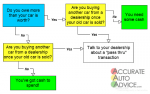

If the total amount of money you owe to your auto lender is more than the value of your vehicle, you have what auto finance people call “negative equity.” This is also known as owning a car that’s “underwater” or “upside down.” This is a pretty common circumstance.

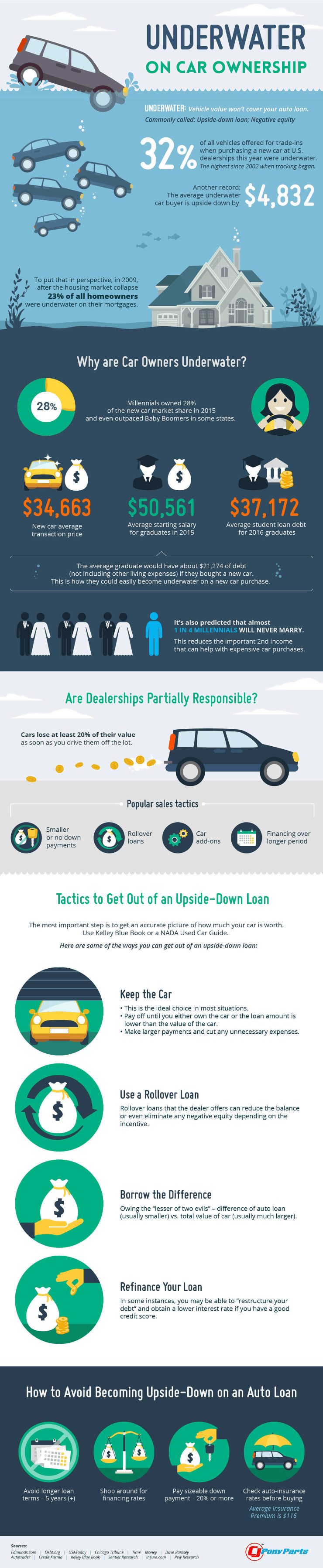

CJ Pony Parts put together a nice looking infographic about negative equity, which is embedded below. While the graphic is nice, it has three key problems:

- The analogy between negative equity and the 2009 housing collapse is a poor one, mostly because cars are depreciating assets and houses aren’t. The 2009 housing collapse was a fairly rare situation where houses everywhere lost value. Cars lose value every day – it’s normal. Negative equity is normal too.

- Dealerships are rarely responsible for negative equity. Every consumer that’s ever gotten a car loan had to sign something to get it – blaming dealers for consumers making poor financial choices is like blaming chefs for obesity.

- The graphic suggests that there are three ways to “get out” of a negative equity situation. In reality, there is only one way; If you have negative equity, you must pay down your loan. Any other solution – rolling over the negative equity into a newer car, refinancing, or a personal loan – is just kicking the can down the road.

If you’re trying to avoid negative equity, the graphic offers some helpful advice:

- Sign up for a 5 year loan term (or less). If you can’t afford the payment over 5 years, it’s probably a good idea to look for a vehicle that’s less expensive.

- Shop around for the best financing. As always, we recommend getting a car loan via your local credit union (or at least investigating that option, as credit unions tend to offer very favorable loan terms).

- Put money down. This is a good idea for a few reasons, not the least of which is that putting money down will reduce your finance charges and save you cash.

Finally, if you’re upside down in your car loan, it’s a good idea to take yourself out of the car buying market for a year or two. Time usually fixes negative equity – the closer you get to the end of your loan, the less likely you are to have negative equity.