A lot of people are uncertain about leasing.

- Part of the problem is that lenders and car dealers make leasing confusing – they have a bunch of special leasing terms, tricks, and information that’s designed to confuse.

- Part of the problem is that a lot of so-called “experts” make blanket statements like “You should NEVER lease” or “Leasing is TERRIBLE.” These types of statements are obviously incorrect.

If you’re thinking about leasing, our advice is to make sure you understand what leasing will mean for you. Don’t listen to some pundit or something your father-in-law told you once about leasing. Take the time to read this guide and decide for yourself.

Here Are The Main Reasons That People Decide To Lease:

- The monthly payment needed to lease a car is usually lower than the payment needed to buy that same car

- Since most leases only last two or three years, people who lease cars usually never have to mess with repairs or most basic maintenance

- Leasing has tax benefits for self-employed people, businesses, and people who can expense vehicle costs

- Leasing is fun – you get to drive a new car every 2-3 years

Here Are The Main Reasons People Do NOT Decide To Lease:

- They drive more than 15k miles per year, which is usually the most you can drive if you lease a car

- They want to spend as little on transportation as possible, and they’re willing to “commit” to a car for a decade as part of that desire to save money

- They don’t understand leasing

To be blunt, the last reason is the biggest. Leasing has a bad reputation, but the fact is that leasing makes an awful lot of sense for a lot of people.

Quick Questions To Figure Out If Leasing Is For You

If you’re thinking about leasing a car, there are 5 quick questions you can answer to decide whether or not you’re a good candidate for leasing:

- Do you like to keep your cars until the wheels fall off? If the answer is yes, don’t lease. Leasing is all about convenience and getting a new car every 2-3 years. If these things don’t matter to you, buying and keeping a car is the way to go.

- Are you trying to maximize every one of your hard-earned dollars? If the answer is yes, good for you…don’t lease. In a purely dollars-and-cents analysis, leasing is almost always more expensive than buying.*

- Have you taken great care of every car you’ve ever had? People who worry about dents and scratches are good leasing candidates. People who don’t notice scratches or dents, torn seats, or carpet stains are not good leasing candidates.

- Do you drive less than 15,000 miles a year? If not, leasing probably doesn’t make sense for you.

- Are you a business owner, self-employed, and/or is someone else paying your vehicle expenses? If the answer to any of these questions is yes, check with your CPA about the benefits of leasing. You’re probably a good candidate for a lease.

*NOTE: If you’ve answered yes to this question, you need to look at the smallest, least expensive vehicle that will meet your basic needs. If you say “I want to maximize every dollar,” and then turn around and buy a $60,000 luxury pickup truck as a commute vehicle…let’s just say that doesn’t make a lot of sense.

Second, Some Terminology

If you’ve answered all the questions above and you’re still reading, the next thing for us to do is define some terms.

Residual Value – Often called the “lease end value”, the residual value is how much money the leasing company believes the car will be worth when the lease is over. Residual values rise and fall based on lease length, lease mileage, vehicle trim level, engine package, etc.

Lease Factor – This is a confusing number that’s basically just an interest rate. Lease factors are used because they are very small numbers – like .00425 – that make the lease interest seem less expensive. If you multiply the lease factor by 2,400, you’ll get the actual interest rate (.00425 = 10.2%).

Gross Cap Cost – This is the total cost of the vehicle, before any rebates, money down, or trade equity are taken out of the price.

Cap Cost Reduction – This is basically the down payment on the lease, minus any up-front fees (like taxes, dealer fees, and first payment).

Net Cap Cost – This is simply the gross cap cost minus the cap cost reduction.

Acquisition Fee – This is the fee that the leasing company charges to “acquire” your lease

Security Deposit – This is usually about one month’s payment, and it’s held by the bank until you return the car. It will go towards paying for any damage, extra miles, or lease termination fees.

WearCare or “Wear and Tear” protection– This is essentially an insurance policy that covers minor damage to your vehicle during the term of the lease. Things like pitted or cracked windshields, worn tires, dents, etc. It’s usually offered in place of a security deposit.

If you’re wondering about a term that isn’t listed here, check out this glossary from the Fed – http://www.federalreserve.gov/pubs/leasing/glossary.htm

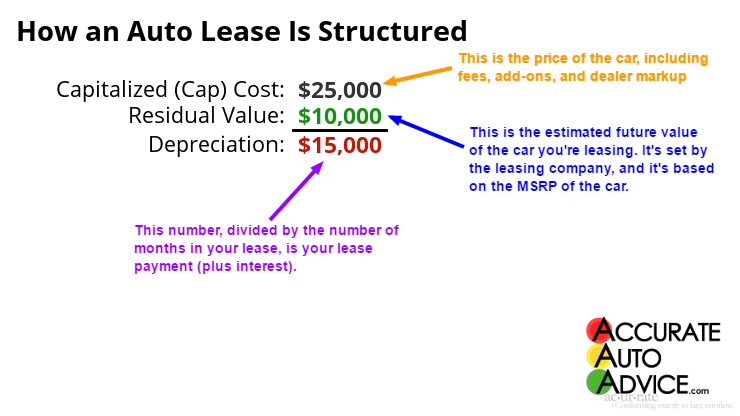

How Auto Leases are Structured

When you lease a car, you’re paying for the right to take the car and drive it for the next 24 or 36 months. During that time, you’re going to pay for the “use” of the car, which is really just the car’s depreciation.

Depreciation is defined as the current value of the car minus the future value. If the car is worth $25000 dollars today, and $10,000 dollars in 3 years, than the depreciation is $25,000 (today’s value) minus $10,000 (the value in 3 years), which works out to $15,000 ($25,000 – $10,000 = $15,000).

The future value (which is $10,000 in the example above) is calculated by the leasing company. This isn’t a number you can negotiate, and it’s usually calculated as a percentage of the vehicle’s MSRP. This percentage is known as a residual value.

Going back to our example above, the depreciation on our 36 month lease is $15,000. However, if we take the depreciation and divide it by 36 months, we don’t quite come up with the lease payment. That’s because the leasing company charges interest on the vehicle while you’re using it, and you’re expected to pay that interest in addition to the depreciation.

The interest rate you pay when you lease a car is going to depend on

- your credit

- the length of your lease

- whatever money you put down on the lease, and

- whatever special offers the leasing company has on this particular car

Also, it’s not technically an “interest rate” that you pay when you lease a vehicle. Instead, it’s a “money factor,” but you can think of them as the same thing. Money factors are usually negotiable, but not always.

Finally, the total cost of your lease is strongly influenced by the up-front cost of the vehicle (aka “cap cost”) and any money you put down when you sign the lease (aka “cap cost reduction”). You can think of a the cap cost as the vehicle price, and the cap cost reduction as a down payment. Both of these things – cap cost and cap cost reduction – are negotiable.

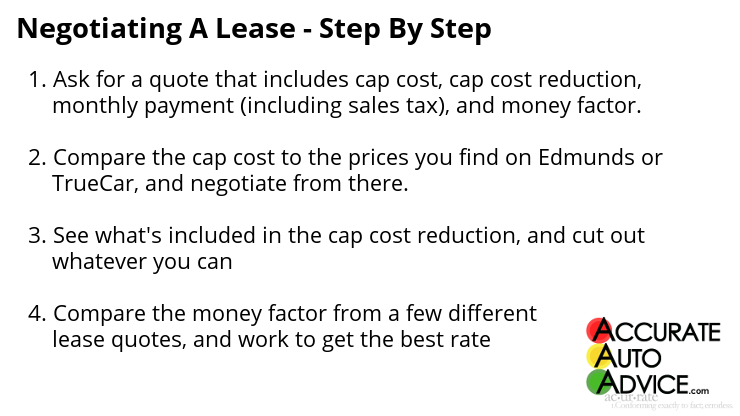

How To Negotiate a Lease

Negotiating a lease is a lot like negotiating a purchase. You just want to change your terminology around.

First, ask the salesperson to show you a quote that lists:

- The exact cap cost, and a breakdown of how that cost is determined (be sure sales tax is included)

- The exact residual value

- The exact monthly payment, including sales tax (sales tax is paid monthly, rather than all up front)

- The money factor being used to calculate the lease payment

If you can’t get a quote that specifies all of the above, go somewhere else. Dealerships that try to hide any of these numbers from you are probably trying to rip you off.

Second, you want to dive into the cap cost and see if you can cut it down.

- The cap cost will include the vehicle price. Compare the vehicle price to Edmunds True Market Value (TMV®) or pricing data from TrueCar. If the price you find online is better than the price shown in the breakdown, ask the dealer to match the best price you can find online, or shop around.

- The cap cost will include various fees. Some of the fees – like title and registration fees – are non-negotiable. Some, like dealer prep and handling, vehicle return fees, or lease buyout fees, can be waived or negotiated down.

- The cap cost may include add-ons or extras like “wear and tear protection”, anti-theft protection, tire and wheel insurance, vehicle paint protectant, etc. You can decide on these extras on your own, but most of them are completely unnecessary. With the exception of wear and tear protection, we don’t recommend buying any add-ons.

Once you’ve worked on the cap cost, the next thing to do is evaluate the cap cost reduction. This is basically a down payment on the lease, and will typically include the following:

- The first payment of the lease. This is normal – you need to pay the first payment before you can take the car.

- Some amount of money down. As far as AccurateAutoAdvice.com is concerned, you should never put money down on a lease unless the bank requires it. Ask the dealer if the lender is requiring you to put money down, or if they can refigure the lease without a down payment.

- Any rebates or special lease cash that’s available from the manufacturer. Most new cars have some lease cash available – the more you get, the better.

- The lease security deposit. Unless the lender requires a deposit- or makes you pay a higher interest rate if you don’t make a deposit – ask to have this removed. The less you put down, the better.

Last but not least, we come to the lease interest rate or money factor. It’s difficult to determine if the lease factor is reasonable or unreasonable without comparison shopping. Therefore, you probably want to ask a few dealers for lease quotes, compare the money factors, and then try to get the lowest rate.

Leasing “Gotchas” – What To Watch Out For

Part of the reason that consumers are so concerned about leasing is that, in the past, dealers used leases to take advantage of consumers. To protect yourself, it’s important to pay attention to the following when leasing a car:

Fees. With leases, you have to be on the lookout for hidden fees. They’ll usually be hiding in either the cap cost or the cap cost reduction, so be sure to ask for a breakdown of these two costs.

Don’t terminate early. While it is possible to get out of a lease early, it’s usually difficult and/or expensive. This is also true of buying a car, but unlike an installment loan, there’s often a penalty for ending a lease early.

Used car leasing is risky. You may see used car leases being advertised, but they very rarely make financial sense. Unlike new cars, a used car lease payment is nearly the same as a used car purchase payment. Therefore, there’s usually very little reason to lease a used car.

Long term leasing. Technically, any lease over 39 months is considered long-term. The biggest problem with these leases is that vehicles need quite a bit of maintenance after 36 months (tires, brake pads, various scheduled service items), and those costs eat up any monthly payment reduction.

Lease return costs. When you return a leased vehicle, the leasing company will inspect the vehicle for damage. While normal wear and tear is expected, this term “wear and tear” isn’t always well defined. It’s a good idea to review lease return rules and make sure you know what to expect when it’s time to turn your vehicle back in.

NOTE: When returning a lease, it’s important to make sure your windshield has no cracks, that the vehicle has no substantial body damage, and that the vehicle is at or under mileage. If it isn’t, you’ll either want to fix these items or explore buying out the lease.

Auto insurance limit requirements can be higher for leased vehicles. In many states, the legally required minimum coverage is lower than the coverage required by the leasing company. The higher coverage requirements could lead to a rate increase (albeit a small one).

The quoted lease payment doesn’t include sales tax. Some dealerships will quote a lease payment that doesn’t include sales tax, as taxes are collected every time a payment is made. Depending on your sales tax rate, the cost of sales taxes can be a shock when the first payment comes.

Don’t lease a car planning to buy it out at the end, at least not unless you’ve plugged all the math into a spreadsheet. While there are situations where leasing a car today and buying it in 2 or 3 years is financially sound (such as when the lease is heavily subsidized by the vehicle manufacturer), this is the exception and not the rule. Leasing a car for 3 years, and then turning around and buying it at the end of the lease on a 5 year loan (for example) means you’re making payments for 8 years. That’s too long.